Blog post

Floating offshore wind (part 1): Coming of age

Energy Blog, 7 September 2017

Martin Guzzetti discusses the strategic rationale behind floating offshore wind, exploring the similarities and differences with fixed-bottom offshore wind projects.

Floating offshore wind (FOW) is coming of age. The first large scale prototypes of FOW turbines have been in operation for several years, and some have already been decommissioned. Demonstration continues for new foundation concepts, while the first commercial FOW farm, Hywind (30 MW) will begin operation off the coast of Scotland by the end of the year. Meanwhile, serious development efforts are happening for large scale FOW farms across the globe, and full commercialisation of the technology is anticipated in the coming years.

The benefits and potential of FOW are indisputable. It can reach areas with better wind resources, it helps limit construction and maintenance activities at sea (which are always more dangerous and expensive than work onshore) and it has a lower impact on the marine environment than fixed-bottom offshore wind. FOW allows construction of utility-scale offshore power plants in countries and areas that would not otherwise be able to do so as water depths get too high too close to the shore, like Japan, California or the Mediterranean basin, where renewable energy alternatives are also either unavailable or reaching a saturation point.

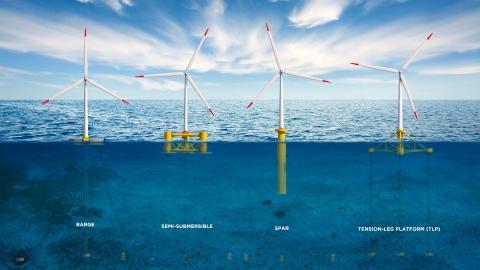

There are presently four FOW foundation concepts: the barge, the semi-submersible, the spar buoy and the tension-leg platform.

Figure – The four floating offshore wind concepts

The first three are connected to the seabed with a relatively slack system of mooring lines and anchors, allowing for an easier installation, while requiring substructure buoyancy or ballast stabilization solution. On the contrary, the tension-leg platform accepts a lighter substructure as it is forcefully connected to the seabed through tensioned tethers, installed via a more complex procedure.

The technology readiness levels of the semi-submersible and spar buoy substructures are currently seen as stronger, as full scale prototypes (mostly 2 MW turbines) have been installed and tested successfully. While several technology providers are currently competing to develop these different types of floating substructures, there is a high probability that a “winner takes all” outcome will occur, with one or two of the more mature technologies (either or both the semi-submersible and spar buoy concepts, as they are best suited to quite different site conditions) prevailing once the early projects are seen as successful, as was the case with monopiles in the fixed-bottom offshore wind sector.

More generally, FOW is following the pathway of the fixed-bottom projects, just as offshore wind followed the footsteps of onshore wind, moving from the R&D stage to prototypes to early stage, small scale commercial developments, to individual full scale projects and finally large scale deployment across several countries. However, there are differences between how the traditional offshore wind sector reached its current status and the course that FOW is experiencing.

The North Sea region provided a perfect incubator for the development of the fixed-bottom offshore wind technology: a shallow basin between countries all looking to swiftly de-carbonise their economies and willing to pay for it, relatively uniform site conditions facilitating the progress of foundation technology (monopiles, jackets and tripods) and an existing supply chain with reasonably relevant expertise and capabilities coming from the traditional marine civil industry (e.g. dredging, port construction, coastal protection) and the offshore oil and gas business.

The sector was also lucky in the sense that the critical early technical and financial precedents took place before the 2008 financial crisis and thus lenders and investors were able to continue to fund the sector even as they retreated from other activities.

FOW is different, in that its development must be supported by countries which have a need for utility-scale renewable power generation which cannot be provided by onshore wind or solar (due to unsuitable resources, or local hostility) or fixed-bottom offshore wind (due to water depths). These countries must also have the political support (or high power prices) to provide the price support which is indispensable in the early days of a new technology. These likely breeding grounds for FOW include the countries facing the European Atlantic and Mediterranean coasts, the US West coast, Japan, the Republic of Korea and Taiwan. None of these areas benefits from the same concentration of available facilities as the North Sea in terms of ports, shipyards, dry-docks and supply chain capacity, and there will be a strong need for lateral investments (which require public support or at least encouragement) to foster technology advancement, improve the coastal infrastructure capacity, and, where relevant, support the necessary onshore grid upgrades and transmission extensions. These countries will not be able to attract financing as easily as the North Sea basin countries which were all seen as reliable, stable, creditworthy and investor-friendly jurisdictions with a strong political consensus to pursue renewable energy, even if relatively or apparently more expensive in the short term (we will discuss financing in a second post).

Additionally, as the governmental approaches towards renewables in these geographies are somewhat diverse (with sometimes very different approaches to issues such as decarbonisation, energy independence, development of the local supply chain, or limiting the cost to taxpayers or ratepayers), with different timelines, the FOW industry may not as easily benefit from the economies of scale the fixed-bottom industry was able to create in the relatively homogeneous North Sea basin.

Finally, FOW may also, a bit unexpectedly, suffer from the short drop in the cost of fixed-bottom offshore wind. While some of the items that drove costs down will directly benefit FOW (like cheaper and more reliable large scale turbines), the price levels achieved in recent European auctions will create a target level that will not be achievable by early FOW projects and this may create the perception amongst governments and regulators, if too impatient, that FOW is too expensive to be worth the effort.

It thus appears that FOW is at a “make-or-break” time – having reached technical maturity, it now needs to demonstrate commercial viability. The willingness of lenders and investors to support the sector will be critical in that respect and will be discussed in a second post to be shortly released.

Martin Guzzetti

In part 2, Martin discusses the financeability of floating offshore wind.